By Allan Sloan and Cezary Podkul/ProPublica

Ever since the COVID-19 pandemic struck, the Federal Reserve has gotten plenty of kudos for moves that have helped stabilize the economy, kept house prices from tanking and supported the stock market. But those successes have obscured another effect: the inadvertent impact the Fed’s ultra-low interest rates and bond-buying sprees are having on economic inequality.

Longstanding inequality in the U.S. has been exacerbated by the Fed’s role in touching off a multitrillion-dollar boom in stock markets – and stock ownership is heavily skewed toward the wealthiest Americans.

In contrast, soaring stock prices don’t help people like Wina Tan. Tan, 59, is one of the millions of Americans nearing retirement age whose greatest source of wealth isn’t stocks or equity in a home. Rather, it’s the Social Security checks she expects to start getting once she retires.

Tan, precariously perched on the lowest rung of America’s working class, earns about $25,000 a year as a job coach for adults with special needs near Irvine, California. She’s a single mom and grandmother and can afford food, rent and healthcare only with the help of federal safety net programs.

Her savings account totals around $11,000, most of it from recent tax refunds and stimulus payments. She’s reluctant to risk that money in stocks, so the bull market will probably continue to charge past her.

Meanwhile, thanks to the Fed’s near-zero interest rates, the best rate her credit union could offer was 0.5% for a long-term certificate of deposit. That would mean earning less than $60 a year on her savings while tying the money up for five years.

Tan’s situation is far from unique. Social Security is the top source of wealth for most lower-income households with workers nearing retirement, according to Teresa Ghilarducci, an economist at The New School in New York City who specializes in retirement.

If the guaranteed income stream of Social Security is treated as an asset, she estimates it amounts to 58% of the net worth for near-retirees in the bottom half of the U.S. wealth distribution. Other retirement savings represent only about 11% of their net worth, and stocks are just 1%. (Home equity accounts for most of the remainder.)

Large swaths of Americans like Tan have essentially missed out on any direct wealth increase from the market’s near doubling since its bottom 13 months ago. Rather, the major beneficiaries have been the wealthiest 10% of Americans, who owned 89% of stocks and mutual fund shares held by U.S. households as of year-end, according to Fed statistics. More than half of that – 53% – is owned by the top 1%.

The Fed’s policies have helped generate jobs and reduce unemployment, which was their goal. In the process, however, the Fed has accelerated the decades-long increase in economic inequality by helping increase the wealth of people at the top far more than it has increased the wealth of working-class Americans.

“High-wealth households do much better in a low-rate environment than lower-wealth households do,” Mark Zandi, chief economist of Moody’s Analytics, said. “The low-interest environment increases inequality by increasing the wealth of people who are well-off.”

Zandi noted, however, that less well-off people don’t lose money because of the low rates; they simply don’t do as well as wealthier people.

Home prices have also benefited from the Fed’s easy money policies, and home ownership is much more evenly distributed than stock ownership is. The wealthiest 10% own only 45% of the real estate held by American households, according to the Fed. The remainder is owned largely by middle-class households, for whom home equity is often their biggest source of wealth.

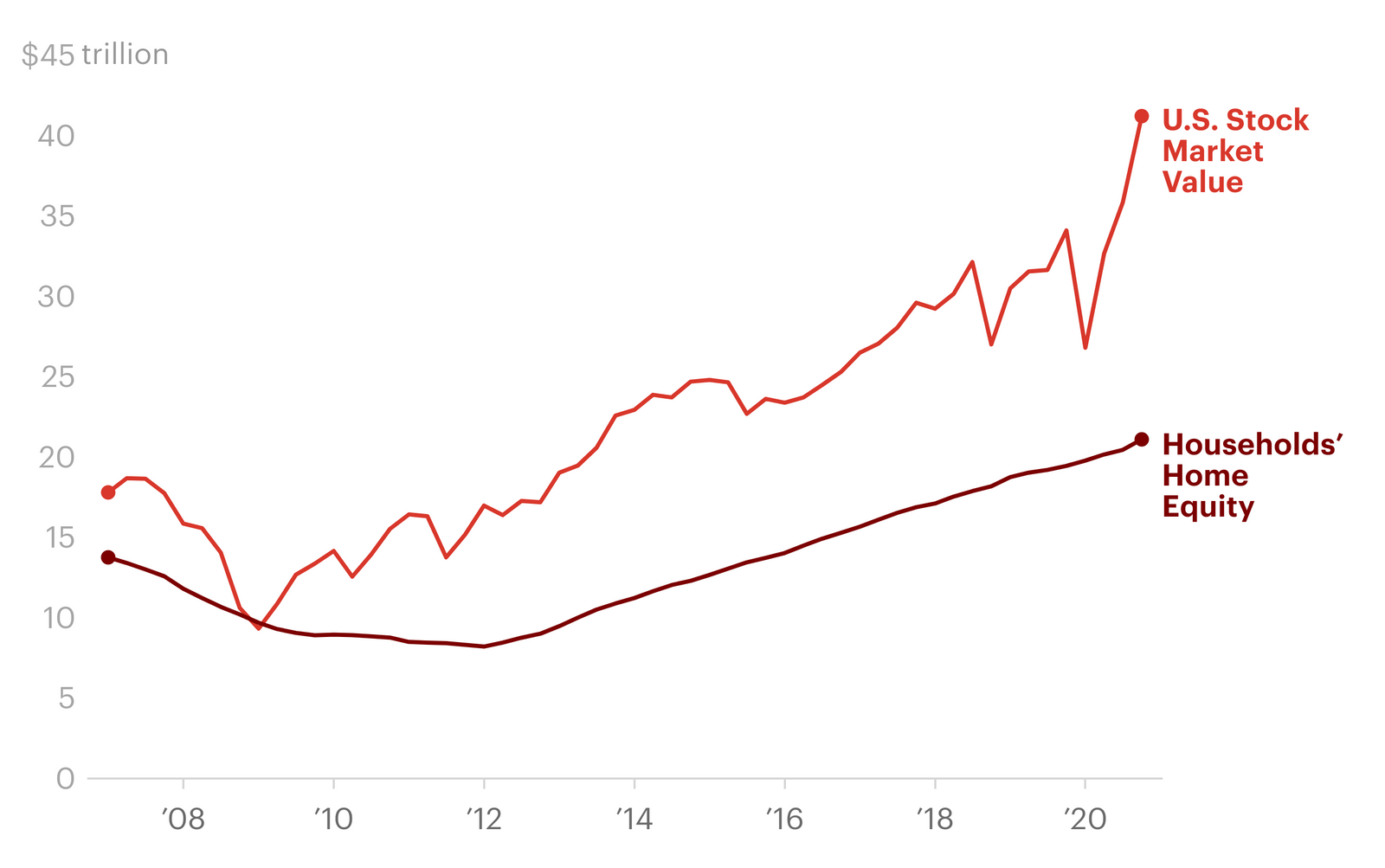

But stock holdings are where the truly massive gains have come. It’s also where there was a big scare last year before the Fed and the CARES Act came to the rescue. COVID-19 sent unemployment soaring and stocks plummeting, as the market fell 35% in 2020 between February 19 and March 23.The market’s rise since then makes the increase in homeowners’ equity look negligible. From last year’s market bottom through mid-April of this year, stocks gained about $22.4 trillion in value, as measured by the Wilshire 5000 Total Market Index.

In contrast, the nation’s total home equity – the value of houses less the debt on them – rose only about $1.3 trillion from the end of last year’s first quarter (eight days after the market low) through Dec. 31, according to the Fed.

Even if you tweak the housing numbers to reflect this year’s gains, or measure the stock market’s gain from before the February drop, the disparity between stocks and home equity is huge.

“Inequality is a cumulative process,” said Karen Petrou, author of The Engine of Inequality: The Fed and the Future of Wealth in America and managing partner of the Washington-based consulting firm Federal Financial Analytics. “The richer you are, the richer you get, and the poorer you are, the poorer you get, unless something puts that engine in reverse,” she said. “That engine is driven not by fate or by untouchable phenomena such as demographics but most importantly by policy decisions.”

Under President Joe Biden, the federal government is trying to both create jobs and funnel lots of money to people like Tan with the $1.9 trillion American Rescue Plan stimulus package. Indeed, Tan is grateful for the $4,200 in stimulus funds she recently received.

“This country has really, really blessed me a lot,” said Tan, a naturalized citizen who emigrated from Indonesia in 1984.

The Biden administration is also pushing for a $2.3 trillion infrastructure bill. But even without a penny yet having been spent on that, the federal government is running up record budget deficits, with more to come.

A considerable part of current and future deficits will be indirectly financed by the Fed, which has been increasing its holdings of Treasury IOUs and mortgage-backed securities by at least $120 billion a month, and has directed its trading desk to increase purchases “as needed” to maintain smooth functioning in the financial markets.

During Donald Trump’s four years as president, the Fed added $2.25 trillion to its holdings of Treasury IOUs, which helped cover the $7.8 trillion of debt the Treasury issued to finance budget deficits during the Trump years. It’s likely the central bank will be the biggest source of finance for Biden’s deficits, just as it was for Trump’s.

Why does that matter? Because when the Fed buys securities, it does so with money that it creates out of thin air. Pumping more money into the financial system increases the money supply, and some of that cash inevitably ends up making its way into the stock market, boosting prices.

Biden is making tax increases a big part of his infrastructure pitch, which in theory would make that legislation less reliant on the Fed. But it doesn’t mean taxes will go up anywhere near as much as he’s proposing. Or that taxes and spending will rise in lockstep. After all, spending is a lot more popular than raising taxes.

Now, let’s step back a bit and see how we got to this point.

During the 2008-09 financial crisis, the Fed initiated “quantitative easing,” a policy under which the central bank buys massive amounts of Treasury IOUs and other securities to inject money into the markets and stimulate the economy. Then-Fed Chair Ben Bernanke championed that approach, which complemented aggressive moves by the Treasury and helped keep giant banks and the world financial system from cratering. (Lots of people still lost their homes to foreclosure, another example of how helping the financial system might not help average people. But that story has already been told.)

Quantitative easing helps stimulate the economy by driving down interest rates, which hurts savers. A telling indicator involves money market mutual funds, where savers have traditionally tucked away spare cash in hopes of earning more interest than bank deposits pay. Money market funds used to produce much more income than stock market index funds. But that ratio began to slip in 2008 and has kept on slipping. At the end of 2007, Vanguard’s federal money market fund was yielding 4.46% and dividends on the Admiral shares of its Total Stock Market index fund yielded 1.78%. (A dividend yield is a fund’s annual dividend divided by its share price.) At the end of 2008, the yield was 1.74% for the money market fund and 2.82% for the stock index fund. The current numbers: 0.01% and 1.28%.

Such low rates have forced average savers to either get by with less interest income or put more money into stocks than they would have otherwise done. That added demand has been one of the factors that has helped push stock prices upward.

Economists are beginning to view the interplay of the Fed’s actions and inequality in a new light. Central bankers used to think that “we didn’t have to worry about inequality when we did monetary policy,” Olivier Blanchard, former director of research for the International Monetary Fund, said during a December virtual forum sponsored by the Peterson Institute for International Economics. Blanchard said he has since come to believe that monetary policy does impact economic inequality because a change in interest rates has “major, major distribution effects between borrowers and lenders, between asset holders and not.”

Spokespeople for the Fed, the Treasury and the White House declined to discuss the impact of soaring stock prices spurred by ultra-low interest rates on economic inequality. So we looked at what some key people involved in the 2008-09 and 2020 Fed bailouts have said publicly.

Fed chair Jerome Powell hasn’t directly addressed the central bank’s role in exacerbating inequality, though he has expressed sympathy for people left behind during the economic comeback. (“There’s a lot of suffering out there still,” he told 60 Minutes in an interview that aired on April 11. “And I think it’s important that, just as a country, we stay and help those people.”)

In a Congressional hearing in February, Powell testified, “We can’t affect wealth inequality . . . We can affect indirectly income inequality by doing what we can to support job creation at the lower end of the market.”

When pressed to discuss problems of wealth inequality by Sen. Elizabeth Warren (D-Mass.), he told her that “those are really fiscal policy issues.”

Bernanke, currently a fellow at the Brookings Institution, acknowledged in a 2017 Brookings paper that “all else equal, higher stock prices mean greater inequality of wealth.” But he maintained that “whatever effects monetary policy has on inequality are likely to be transient, in contrast to the secular forces of technology and globalization that have contributed to the multi-decade rise in inequality in the United States and some other advanced economies.”

Like Powell, Bernanke argued that inequality is the purview of fiscal policymakers (Congress and the White House) rather than the Fed.

Janet Yellen, who was the Fed’s vice chair under Bernanke and is now Treasury secretary, asked in a 2014 speech whether income inequality is “compatible with values rooted in our nation’s history.”

But she largely defended ultra-low rates during a Q&A at a 2013 conference of business journalists. Older savers were “suffering from low returns on their CDs,” she said, but “they have children and they have grandchildren” who will benefit from the stronger economy.

However, the economic effects of quantitative easing eventually fade, according to researchers at the Bank for International Settlements, a Switzerland-based institution that acts as a central bank for central banks. The BIS concluded in a 2017 study that quantitative easing had more success boosting stock prices than boosting economic growth.

Over time, the economic impact trended toward zero while stocks saw a “significant and persistent positive impact,” the researchers found.

Jason Furman, a former chair of President Barack Obama’s Council of Economic Advisers and currently an economics professor at Harvard, summed up the inequality tradeoff this way in an interview: “I don’t want to have a lower stock market and higher unemployment.”

In other words, increasing wealth for the wealthy is an inevitable side effect of keeping interest rates low to support the economy and create jobs.

The latest round of stimulus checks will help close that gap a little by putting money in the pockets of low-income earners like Tan. But near-zero interest rates will make it harder for them to save the money for the future, as Tan hopes to do.

She would like to set aside $1,000 to $2,000 in savings accounts for her 16-year-old son and 3-year-old grandson in addition to saving for her retirement and a rainy-day fund.

And as the Fed pumps more money into the financial system by buying Treasury securities and indirectly supporting federal stimulus programs, the run-up in stock markets is likely to continue – and leave people like Tan even further behind than they already were.

–

Previously by Allan Sloan:

* Beware Wall Street’s Magic Beans.

* Remember Bill Clinton’s Phony Executive Pay Cap? It’s Even Less Effective Than We Knew.

* A Schlupfloch Here, A Schlupfloch There. Now It’s Real Money.

* Carried Interest Reform Is A Sham.

* How The Fed Is Screwing Your Retirement By Taking Care Of The Rich.

–

Comments welcome.

Posted on April 27, 2021